Valuations Killing Home Sales in Queensland

ADC calls for an urgent review by the State Government of Queensland valuation processes

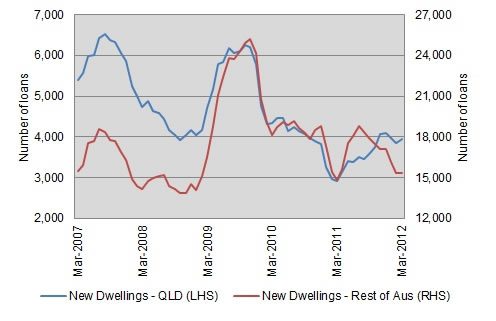

See Below: Brian Stewart (CEO UDIA QLD) presents the latest housing finance figures and offers his assessment of the problems plaguing Queensland’s property valuation system.

Housing finance upward trend

Latest housing finance figures from the Australian Bureau of Statistics show loans to owner occupiers in Queensland were up 2.0% in the month of March and 5% over the full March quarter (seasonally adjusted) – the second strongest quarterly result in the nation behind Western Australia.

Across Australia, loans to owner occupiers rose just 0.3% in March and are down 1.4% over the full March quarter.

Turning specifically to the new home market, lending for the construction or purchase of new homes in Queensland rose a further 4.7% in March, building on the 22.3% increase observed February.

Growth in Queensland lending and building approvals has clearly outperformed the rest of the nation for a number of months now. With sound economic fundamentals in place, low interest rates and rising confidence, the upward trend in Queensland lending and approvals since late 2011 is likely to continue through 2012 and 2013.

Despite the outlook for increased activity, the industry will continue to be unable to deliver an adequate supply of new housing at affordable prices unless bold planning and taxation reforms are pursued as a matter of urgency by all levels of Government.

Chart 1: Owner Occupier new home lending

Original, Moving quarterly total

Valuations killing home sales in QLD

Whenever two or three industry reps get together these days it takes about 5 minutes for the conversation to turn to the vexed question of valuation of new dwellings for the purposes of obtaining finance. So what are people saying?

- Real estate agents and developers blame the valuers;

- Valuers turn ostrich and say that they are simply providing a valuation for a client based on the parameters of the request from the financier, or that the fees paid by Valex for such valuations are at such a low level that valuations are uneconomic to perform in a comprehensive manner;

- The financiers’ answer is that there are requirements from the mortgage insurers that are imposed on borrowers;

- And, the mortgage insurers no doubt assert that they are accountable to their shareholders and need to manage risk and that is harder to do in a falling or steady market than it is in a rising market.

In the latter part of last year and the earlier part of this year UDIA (Qld) undertook research funded by sponsorship from SSKB to ascertain what we believed to be the facts and to identify some solutions to the problem.

Contemporaneously the PCA, HIA and MBA started raising this issue on behalf of builders, investors developers and others. A joint working party was established and a multi-party meeting held with representatives of the Australian Bankers Association (ABA) and the Australian Property Institute (API). It was hoped that this meeting would assist in resolving some of the issues and to ascertain more of the facts. And that is what it did to a degree. Further meetings will be held in the future and it is to be hoped that these will resolve some of the difficulties that have yet to be addressed.

So what is the situation, as I see it, and what needs to be done to address it?

Read Brian’s full discussion here

Download the Valuations paper here

Source:

Brian Stewart

UDIA (QLD)

Chief Executive and General Counsel